What the war with Iran has to do with mortgage rates and how it's affecting our market

- Mar 25

- 2 min read

|

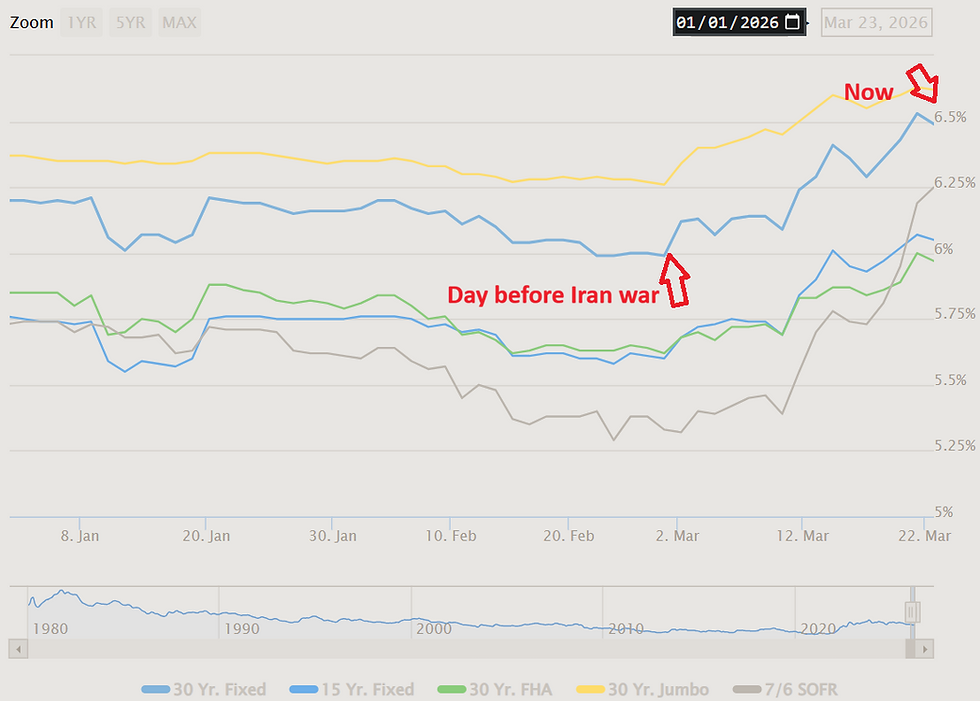

Just as we dipped below 6% on mortgages, a fresh war with Iran sent rates right back up to the mid 6's. Why? Short answer is that it wasn't the war itself - it was what the war did to inflation expectations and the bond market. The war triggered an oil shock, which I am sure you have felt at the pump - I know I have. A disruption in the oil supply touches almost everything: gas, shipping, construction, food cost, my recent road trip budget. Higher oil prices = higher inflation expectations. Inflation is the #1 enemy of bond investors and if inflation is expected to rise, fixed rate bonds (like Treasuries, which are tied to mortgage interest rates) become less attractive. When bonds become less attractive, investors sell bonds or demand higher returns. This pushes the Treasury yields UP, and along with them, mortgage rates. Now that we're done with our Economics lesson (yawn), what does this really mean and how long may it last? Well, a lot depends on how long this war lasts, and when it ends, how long its effects remain. Short conflict = temporary spike in rates. Prolonged conflict = prolonged spike in rates. As of this writing, Trump has signaled nearing a resolution with Iran, which immediately sent oil prices down a tad. But as we know, the markets (and messaging from the Executive branch), can be fickle. If inflation sticks, we are unlikely to see any more cuts by the Fed this year. In fact, they may reverse course again and decide to tick up the Fed funds rate again. We all hope not. What do the buyers out there think? Not much apparently. Boots on the ground observations (which are not yet available in the data and won't be for weeks) show unwavering buyer interest (for now) - very busy open houses this past weekend with active buyers making offers. Although the current situation has visibly impacted things like mortgage refinances (I know I've put mine on hold until rates stabilize again in the downward direction), it seems to be having less impact so far on people needing to move. Data should materialize in the coming weeks that will signal if there is a change in market demand as a result of this conflict, but for now, it appears to be business as usual here - apart from our wallets being emptier after visiting the gas station. Why isn't this having more of an impact? Well, it still might, but 6.5% interest rates aren't a shock to anyone like they were after the initial post-COVID run up in rates. "Been there done that" seems to be the sentiment at the moment, but time will tell. |

Want local data or strategy by city? I’ll send over a quick custom summary for your neighborhood or price point. Let me know what you'd like to see by scheduling a quick call with me or by contacting me here. |

Comments